Business Succession Planning

Business owners spend years—often decades—building their companies.

But many never plan for what happens to that business if something unexpected occurs.

And when there is no plan, decisions may be left to courts, family members, or business partners who may not agree.

What happens if:

- an owner dies

- a partner becomes disabled

- a divorce affects ownership

- an owner wants to retire

- partners disagree on the future

Without a succession plan, businesses can face:

- forced liquidation

- disputes among family members

- ownership conflicts between partners

- tax consequences

- court involvement

A well-designed succession plan helps ensure the business can continue operating smoothly.

What is Business Succession Planning?

Business succession planning is the legal and strategic process of planning for the transfer of ownership and control of a business.

It typically addresses:

- death of an owner

- retirement

- disability

- voluntary sale

- transfer to family members

- partner buyouts

A properly structured plan may include legal, financial, and tax considerations.

Common Succession Planning Tools

Buy-Sell Agreements

Agreements between owners that establish how ownership interests are transferred upon specified triggering events.

Operating Agreement or Shareholder Agreement Provisions

Govern governance and transfer restrictions.

Key Person Insurance

Provides liquidity if a critical owner dies.

Business Trust Structures

Used for family transitions.

Valuation Mechanisms

How the business will be valued for buyouts.

Funding Strategies

Ensuring funds exist to buy out an owner.

Family Business Succession Planning

Family businesses are often built over decades—but without proper planning, they can face serious challenges when ownership transitions to the next generation.

Succession planning for family-owned businesses involves more than simply transferring ownership. It requires careful coordination of legal, financial, and personal considerations to protect both the business and the family relationships behind it.

Common issues include:

• transferring ownership to children or family members

• balancing interests between active and non-active heirs

• protecting the business from disputes among family members

• addressing fairness versus equality in distributions

• minimizing tax consequences and preserving business value

Without a clear plan, transitions can lead to conflict, operational disruption, or even the loss of the business.

A well-structured succession plan helps provide clarity, continuity, and long-term stability—ensuring the business you built can continue for future generations. Without planning, even strong family relationships can become strained when business and inheritance issues collide.

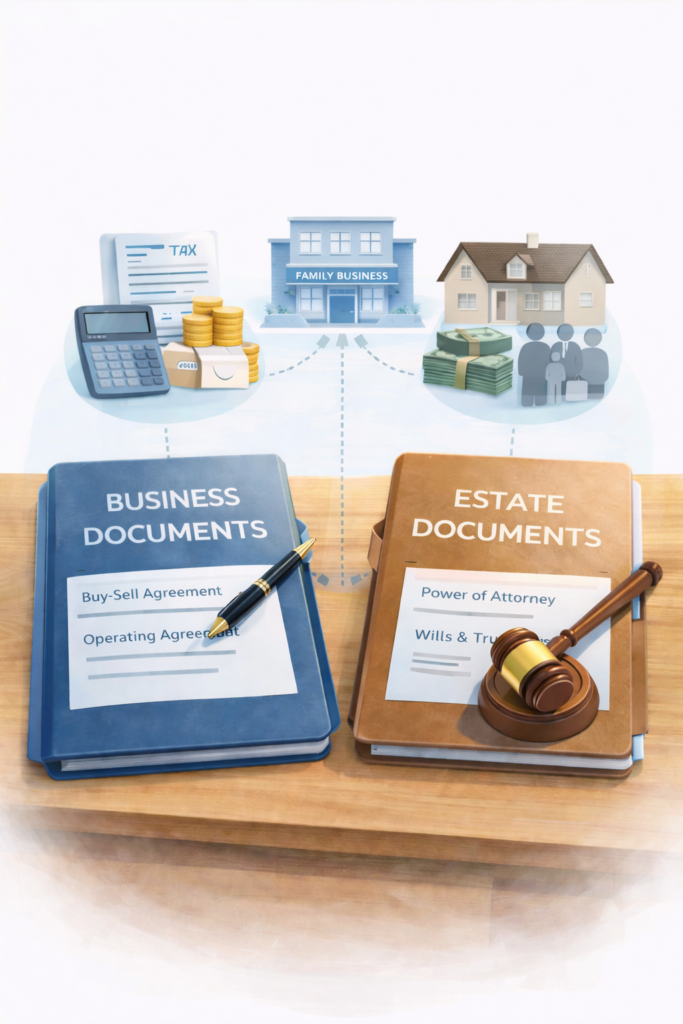

When Estate Planning and Business Succession Planning Intersect

For business owners, estate planning and business succession planning are closely connected—and should be carefully coordinated.

A business is often one of the most valuable assets in an estate. Without proper alignment between business documents and estate planning strategies, unintended consequences can arise.

A comprehensive plan may coordinate:

• ownership transfers of business interests

• trusts designed to hold or manage ownership

• tax planning strategies to minimize estate and transfer taxes

• management control and decision-making authority

• asset protection for both the business and family members

If these elements are not aligned, conflicts can occur between operating agreements, buy-sell provisions, and estate planning documents—potentially leading to delays, disputes, or unintended transfers.

Proper coordination helps ensure that ownership passes as intended, the business can continue operating without disruption, and both business and family interests are protected. These issues are not always obvious—and often only become apparent when it is too late.

Protect What You’ve Built. Plan What Comes Next.

If you own a business and have not developed a succession plan, now is the time to take a closer look.

A well-structured plan can help protect your business, your family, and the value you’ve worked hard to create.

Schedule a consultation today to begin building a strategy tailored to your business and your goals.

Frequently Asked Questions

What is a business succession plan?

A business succession plan is a legal and strategic plan that outlines how ownership and control of a business will be transferred in the event of retirement, disability, death, or sale. It helps ensure continuity of operations while protecting the interests of owners, employees, and family members.

Why is business succession planning important?

Without a succession plan, businesses may face disputes, operational disruption, financial loss, or even forced liquidation. Proper planning helps maintain continuity, preserve business value, and ensure ownership transfers according to the owner’s intentions.

When should a business owner create a succession plan?

Business owners should begin succession planning as early as possible. Unexpected events can occur at any time, and early planning provides more flexibility, better tax strategies, and smoother transitions.

What happens to a business if the owner dies in Florida?

In Florida, what happens to a business when an owner dies depends on the business’s governing documents and the owner’s estate plan. Ownership interests may pass according to a buy-sell agreement, operating agreement, or trust. If no plan is in place, the ownership interest may be subject to probate, which can result in delays, disputes, or unintended transfers.

What is a buy-sell agreement and why is it important?

A buy-sell agreement is a legally binding contract between business owners that establishes how ownership interests will be transferred upon specified triggering events, such as death, disability, retirement, or voluntary sale. It helps provide clarity, reduce disputes, and ensure continuity of the business.

How does business succession planning work with estate planning?

Business succession planning and estate planning serve different but related functions. Business documents govern whether and how ownership interests can be transferred, while estate planning documents determine who receives those interests. Coordinating both helps ensure transfers are legally valid and consistent with the owner’s intentions.

Do small and mid-sized businesses need succession planning?

Yes. Succession planning is important for businesses of all sizes, including closely held and family-owned businesses. Even mid-sized businesses can experience significant operational and financial disruption without a clear plan in place.

Can a business be transferred to family members?

Yes, but transferring a business to family members requires careful planning and must comply with the business’s governing documents. Issues such as management control, fairness among heirs, tax considerations, and long-term sustainability should be addressed to help ensure a successful transition.

How is a business valued for succession planning?

Business valuation methods vary depending on the type of business and the terms of any governing agreements. Common approaches include agreed-upon formulas, independent appraisals, or periodic valuations. The appropriate method is often defined in a buy-sell agreement.

Do I need a business succession plan in Florida if I already have an estate plan?

Yes. An estate plan alone does not control how ownership interests in a business may be transferred under the business’s governing documents. In Florida, business succession planning should be coordinated with estate planning to help ensure ownership transfers are valid, enforceable, and consistent with the overall plan.